The housing and stock markets continue to be the leaders in the economy. In August, showings and pending sales remained at strong levels while housing inventory remained limited, continuing the competitive bidding market we have seen in recent months. With the stock indexes at or near record highs as mortgage rates remain near record lows, signs point to a busy fall housing market.

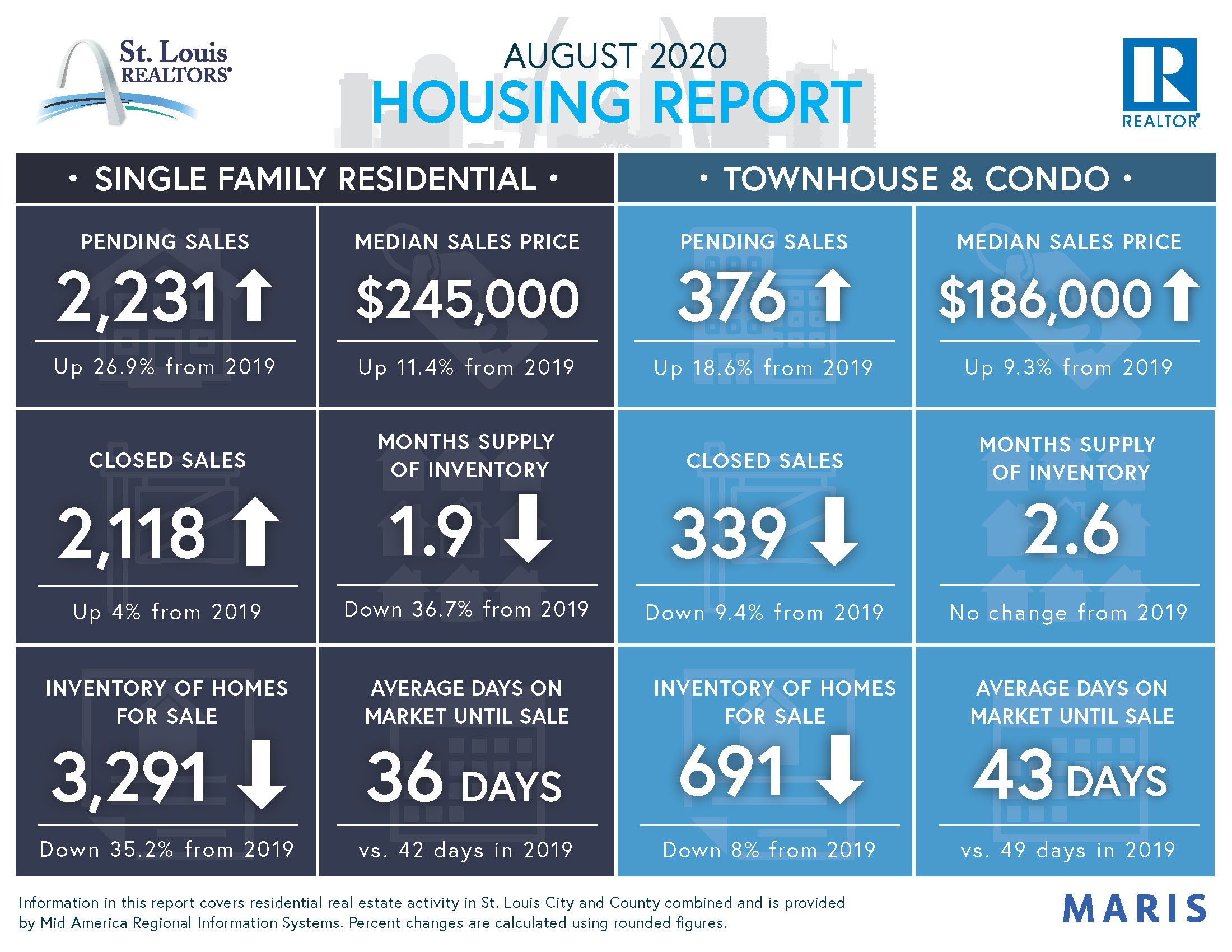

New listings decreased 2.3 percent for residential homes but increased 3.9 percent for townhouse/condo homes. Pending Sales increased 26.9 percent for residential homes and 18.6 percent for townhouse/condo homes. Inventory decreased 35.2 percent for residential homes and eight percent for townhouse/condo homes.

Median sales price increased 11.4 percent to $245,000 for residential homes and 9.3 percent to $186,000 for townhouse/condo homes. Days on market decreased 14.3 percent for residential homes and 12.2 percent for townhouse/condo homes. Months supply of inventory decreased 36.7 percent for Residential homes but remained flat for townhouse/condo homes.

As we look towards the fall, we normally see housing activity begin to slow a bit as the back-to-school season begins, but this year is far from normal. While uncertainty remains on what effects the upcoming elections and any seasonal resurgence of COVID-19 may have on the financial and housing markets, the healthy housing demand we see today will create significant tailwinds in the near term.

July Opportunities