In November, the Federal Reserve reduced its benchmark rate for the third time this year. This action was widely anticipated by the market. Mortgage rates have remained steady this month and are still down more than one percent from last year at this time. Residential new construction activity continues to rise nationally. The U.S. Commerce Department reports that new housing permits rose five percent in October to a new 12-year high of 1.46 million units.

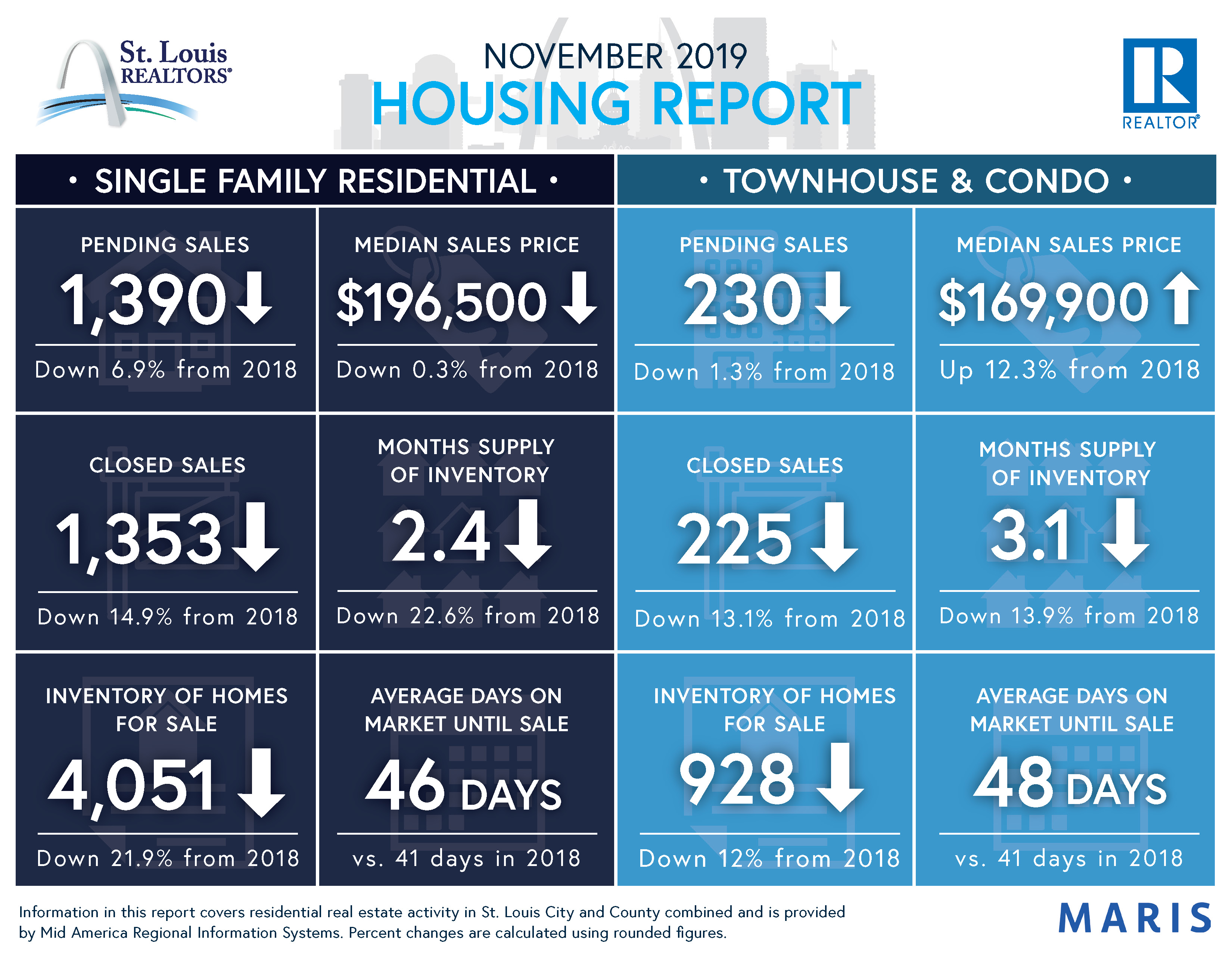

New listings decreased 0.1 percent for residential homes but increased 2.7 percent for townhouse/condo homes. Pending sales decreased 6.9 percent for residential homes and 1.3 percent for townhouse/condo homes. Inventory decreased 21.9 percent for residential homes and 12.0 percent for townhouse/condo homes.

Median sales price decreased 0.3 percent to $196,500 for residential homes but increased 12.3 percent to $169,900 for townhouse/condo homes. Days on market increased 12.2 percent for residential homes and 17.1 percent for townhouse/condo homes. Months supply of inventory decreased 22.6 percent for residential homes and 13.9 percent for townhouse/condo homes.

While many economic signs are quite strong, total household debt has been rising for twenty-one consecutive quarters and is now $1.3 trillion higher than the previous peak of $12.68 trillion in 2008. While delinquency rates remain low across most debt types (including mortgages), higher consumer debt loads can limit future household spending capability and increase risk if the economy slows down.

Opportunities November 2019